The Real "Debt" Crises Congress Ignores

While the media focuses another fight over the debt ceiling, Congress plays politics with the impending bankruptcies of Social Security and Medicare. Is it too late to avoid serious pain?

Debt ceiling debates are a dime a dozen in Washington, DC. Unfortunately, fixes to what causes them - deficit spending - are not.

And then there are the massive drivers of federal spending outside Congress’s budgetary control, so-called “mandatory spending.” Those include Social Security, Medicare, Medicaid, and a host of other programs, including food stamps, the Earned Income Tax Credit (EITC), child nutrition, and more.

The total cost of these mandatory programs - comprising about 70 percent of all federal spending - is around $5 trillion annually. And never mind the issue of unfunded liabilities.

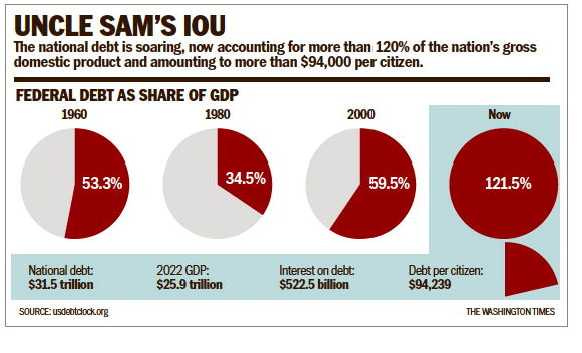

Federal debt is now at $31.4 trillion. That’s twice the level from the last major debt ceiling “crisis” in 2011 (there was a mini “crisis” in 2013 and again in 2017). Most of these “crises” were resolved with agreements to raise the debt ceiling in exchange for various and sometimes vague or complicated spending reduction schemes. In 2011, “budget sequestration” was introduced, calling for automatic across-the-board spending reductions for defense and non-defense discretionary programs equal to increases in the public debt. It was painful, harmed national defense, and didn’t work well.

Republicans typically support higher defense spending, while Democrats prefer domestic programs. Each side has tended to resolve its differences by agreeing to a trade-off, in case you wonder why we have a $31.4 trillion deficit. The deficit was $1.4 trillion alone in Fiscal Year 2022, which ended last September. That works out to about $4 billion of borrowing every day.

And that was before Congress passed its $1.7 trillion pork-laden Consolidated Appropriations Act last December.

With its power of the purse, Congress finds debt ceilings useful, providing leverage over the Executive branch on spending priorities. However, it often results in many wrong ideas and political shenanigans. A divided Congress, as we have now, makes this especially challenging.

Bad ideas are re-emerging. One is eliminating the debt ceiling so we don’t have these dramatic, politically-charged interludes. Given the media’s awful and frequently hysterical coverage, it’s very tempting. But that also eliminates a tool to help focus public attention on our ballooning federal deficit.

Another bad idea is minting a $1 trillion (or more) Platinum coin. Fortunately, Treasury Secretary Janet Yellen has spiked that nutty gimmick. Using its power to mint coins, the Treasury would establish a new platinum coin, assess its value at whatever, and deposit it with the Federal Reserve (which might not accept it). It’s a gimmick by an Atlanta lawyer named Carlos Mucha via an economic blog. The Obama Administration briefly considered and rejected the idea.

The third bad idea is evoking the 14th Amendment’s clause that the validity of America’s public debt “shall not be questioned.” Under that theory, the Executive could ignore the debt ceiling and issue bonds to avoid default, citing the Constitution’s supremacy. That would certainly wind up at the Supreme Court while a Damocles sword hangs over all those bonds whose validity would be in doubt.

Here’s the thing: everybody in Congress agrees the debt ceiling must be increased. House Republicans want yet-to-be-outlined spending cuts and reforms as part of any debt ceiling increase, as they’ve done before (how has that worked out?). Democrats, who are not interested in spending cuts, are raising strawmen and outright falsehoods such as cuts to Social Security, Medicare, and Medicaid as the GOP agenda. Democrats got a boost from former President Trump, who called on the GOP not to reduce benefits in those programs they have never proposed.

And interest payments on the federal debt - not including principle - exceeded $50 billion per month during the first two months of this fiscal year (October and November 2022). At that rate, some $600 billion will be spent to service the existing debt, never mind what’s coming. That’s approaching $2 billion per day just for interest on federal debt.

Some seek to blame the so-called Trump tax cuts for the deficit - some even go back to the Reagan-era Economic Recovery Tax Act - that slashed tax rates for most Americans. Still, federal revenues have continued to rise under both. The problem is spending, not taxes (although tax simplification and reform would be welcome).

Meanwhile, the Congressional Budget Office said last month that the Old Age, Survivors, and Disability Insurance (OASDI) trust fund that pays Social Security retirement benefits would go bankrupt by 2033 - in ten years. That trust fund pays Social Security retirement benefits to over 50 million Americans (and growing) over age 62 (plus an additional 20 million beneficiaries as the program has been expanded). Payments are flowing out of that trust fund faster than revenue is flowing in. The Medicare Trust Fund goes belly up at the same time.

My friend and former Social Security Trustee, Dr. Charles Blahous, has warned of this for years.

What does this mean? Sometime in 2033, the trust fund will only be able to pay 76 percent of promised payments. That will mean - barring action from shoring up the trust fund by Congress and the President - an immediate 24 percent cut in Social Security retirement benefits. Same for Medicare.

Good luck with your doctor when that happens. You may think that Congress will never let that happen. Are you sure about that? Seen Congress lately?

By the way, while Social Security claims to have some $2.9 trillion in assets, they’re all invested in government bonds. That trust fund consists of nothing more than government IOUs. Congress and past Administrations have been borrowing from the trust fund since it was created. Some people believe that all the money they and their employer (a combined 15%) have paid into the OASDI trust fund all these years were put into an account with their name on it, and when they retire, they start collecting on it. No, it has always been an inter-generational transfer program where workers subsidize Social Security recipients.

Some will claim that ten years is several political lifetimes and Administrations away. Untrue in this case. The time to address this problem was in 2005 when President George W. Bush proposed a fix that would have been less painful. Democrats excoriated him for it (along with a botched Hurricane Katrina response that year), and the GOP lost control of Congress in the next election.

Any political will to fix a growing problem evaporated and has yet to return, resulting in an unprepared public. When Donald Trump ran for President in 2016, he promised never to touch Social Security and Medicare. It may have been good politics, but it kicked the can down the road into a dark, dangerous alley. He still talks that way.

We are now at a point when any fix is painful and politically challenging. It most certainly will include phasing in a new full retirement age to 70 for anyone under age 55, lifting the wage cap for paying Social Security taxes (currently $160,200, adjusted annually), and possibly changing the index by which benefits are increased.

Benefits are adjusted based on a “wage” index. Moving it to an index based on inflation alone, instead of wages, should slow future increases. And this might not be enough.

Means-testing (people making a certain income wouldn’t qualify for benefits) has already crept into the discussion. That would convert Social Security from an “income transfer” program that pays for itself into a welfare program. Some say it already is.

Many Democrats will insist on tax increases, but demagogue that raising the retirement age or adjusting indexed increases are “benefit cuts.” Democrats want to expand these costly programs. They have proposed lowering the age to qualify for Medicare to age 60 and expanding other benefits, such as vision and dental, despite its impending bankruptcy. But their politicizing and poisoning even a discussion is, in effect, foretelling an immediate 24 percent cut in 10 years. Maybe sooner.

Every time you hear a politician attack or criticize even a discussion of rescuing these trust funds, ask them this: “So, you favor an immediate 24 percent cut in benefits?” That’s where we’re headed.

One way to start a serious bipartisan discussion would be to include the TRUST Act as part of any debt limit increase. It doesn’t, on its face, do anything, but it would create “rescue” committees to address trust fund issues that drive much of our debt and fast-track solutions to Congress for votes. Meanwhile, our periodic game of budgetary chicken is underway. It rarely ends well. D-Day arrives sometime early this summer, and Congress rarely acts until it has to.

House Republicans reportedly are now considering a “clean” debt limit increase tied to the end of the fiscal year (September 30th) to buy time and create leverage for the annual 12 major appropriations bills, coupled with a possible “reconciliation” tax bill. That’s an intelligent strategy if they can make it work.

Americans are on board with reductions in spending as part of any debt ceiling increase, theoretically and for now. However, pollsters rarely ask about specific spending cuts (“No! Not THAT!”). And count on Democrats to demagogue any specific spending cuts, even eliminating plans to hire an additional 87,000 IRS employees over the next five years. Meanwhile, several Trump-era Tax Cuts and Jobs Act provisions are expiring this year.

I was a young congressional aide in 1983 when President Reagan, House Speaker Thomas P. O’Neill, Senate Majority Leader Bob Dole, and a handful of others crafted a compromise that rescued Social Security until now. It phased in a retirement age hike up to age 67 for workers under age 50, modestly phased in higher tax rates and other reforms. It was bipartisan, it wasn’t politicized, and it worked. Best of all, their bipartisan statesmanship helped sell the public on the urgent need.

They also warned that it would not last forever, especially as baby boomers born between 1946 and 1964 began to retire. Some 10,000 people turn age 65 every day.

Where are President Reagan, Speaker O’Neill, and Senator Dole when we need them?

Some may be stepping up, at least quietly and behind the scenes, accompanied by the usual demagoguery. From the New York Sun’s Scott Norvell:

Last week, reports surfaced that two senators, independent Angus King of Maine and Republican Bill Cassidy of Louisiana, have been meeting behind closed doors to map out potential ways to shore up the program. Among the ideas, according to Semafor, is the creation of something akin to a sovereign wealth fund as a backstop to the existing Social Security Trust Fund.

Among Democrats in the Senate, the idea getting the most traction is one described by Mr. Manchin as the “quickest and easiest” for Congress in the short term — raising the cap on the payroll taxes currently used to fund Social Security. Currently, only wages up to $160,200 a year are subject to the taxes.

Senator Sanders of Vermont said he would be introducing a bill doing just that, one that he insists would simultaneously extend the program’s solvency by 75 years and increase benefits. “Today, a billionaire pays the same amount into Social Security as someone making $160,000 a year,” Mr. Sanders said on Twitter. “Let’s end that absurdity.”

What’s a “sovereign wealth fund?” This will help answer that.

Sadly, the Reagans, the O’Neills, and the Doles are gone. Will successors with the courage emerge? We’re in for a world of hurt unless and until they do - and soon.

On behalf of Generation X, thanks for nothing to our gutless politicians. The system we have been forced to pay into for our entire working lives will now go broke just before we would have qualified for full benefits. Great job, everyone 👏🏻