How One Biden Tax Proposal Will Hit the Middle Class. Good and Hard.

It's Called Eliminating "Step-Up Basis"

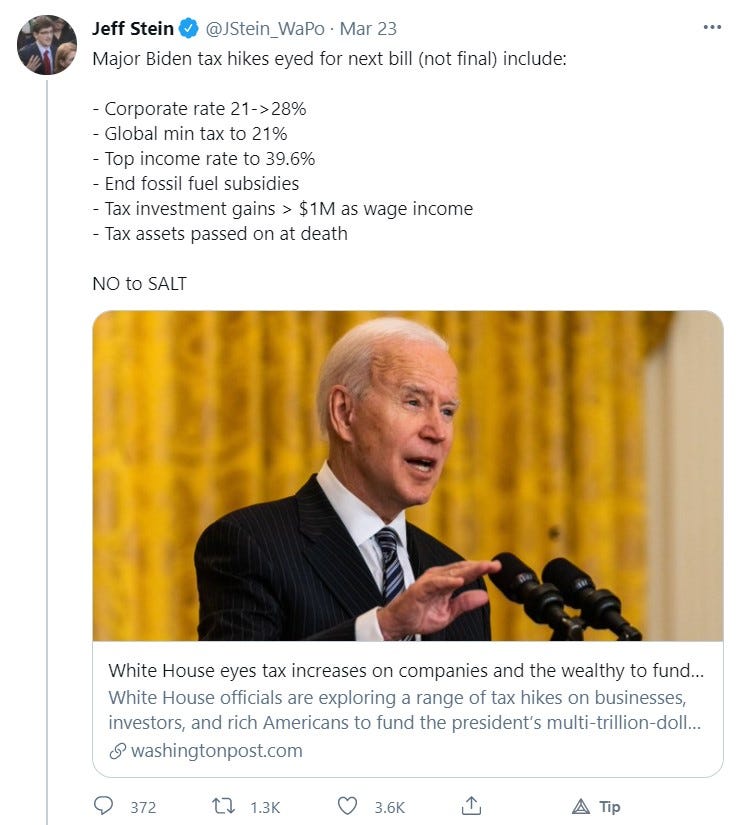

We haven’t seen details of President Biden’s “Made in America Tax Plan.” It’s designed to pay for his $2 trillion “infrastructure” plan. All we have is an 18-page description published by the Department of the Treasury. But it’s a good guess that we will get all the details when the White House finally sends its FY2022 budget and supporting materials to Congress, likely after he finally delivers his first State of the Union (SOTU) address before a Joint Session of Congress on April 28th, right before his 100th day in Congress. That’s a popular but meaningless benchmark that journalists like to write about.

But one needs to go back to the 2020 campaign and read or hear what then-candidate Biden promised as part of his tax plan. We know that he promised to repeal the “Trump Tax Cuts” that lowered tax rates for everyone and really lowered corporate income tax rates from the world-highest 35% to 21%. Biden also promised not to raise taxes on incomes of less than $400,000 per year.

But one thing to remember: terms and phrases are redefined constantly by progressives. Consider this, from US Rep. Mondaire Jones (D-NY):

I guess it might qualify to the extent that the Supreme Court building would need some renovation if Democrats packed the court with four new justices.

You’re going to hear a lot about how this is focused on “taxing the wealthy,” and that may sound fine. After all, many wealthy corporate types have gone all woke, so I’m not interested in coming to their defense.

This isn’t about them. This is about me. And you.

Do you really believe it when Democrats say incomes of less than $400,000 won’t be touched by Biden’s tax plans? That actually is not true since, as we know, corporations do not ultimately pay taxes - they collect them. From you. Please carefully note what they say and don’t say their “promise” includes, such as intergenerational transfers of property and assets, like houses, family businesses, family farms, and stock.

Meet step-up basis. It is very dangerous for me to discuss taxes, but here’s how that works (click the links for more expert examples). Say you’re a 60-year-old almost-retiree whose 90-year-old parent just passed away. My sympathies. That parent had a will and bequeathed you their Florida beach condo that they acquired in 1980 for $100,000 mortgage-free. The value of that nice condo is now $500,000. Hopefully, it won’t be complicated by a reverse mortgage or isn’t burdened by other forms of debt leveraged by the value of that property.

You don’t want the condo and need the money for retirement, so you decide to sell it to pocket the cash or reinvest it. The condo sells for exactly $500,000. Thanks to “step-up basis,” you will owe no federal Capital Gains tax on the sale. But what if Biden accomplishes his promise to eliminate the step-up basis “loophole?” You’ll owe capital gains taxes on the gain in value since your parent bought the property 41 years ago, most of which is probably inflation, which won’t matter. That’s a likely 20% tax hit on the “gain” (assuming Biden and his fellow Democrats don’t touch Capital Gains tax rates) of $400,000 - some $80,000 to Uncle Sam. For people with incomes over $1 million, word has it that Biden will raise Capital Gains taxes to match the highest personal income tax rate of 39.5%. Again, maybe you’ve not fazed, but don’t expect that number to be adjusted with inflation.

Government causes inflation but taxes you for it.

Also, there’s talk that the Biden plan may exempt the first $1 million of “unrealized” gains, so there’s that, but that’s a shallow threshold for a family business or a farm. But don’t count on it being indexed for inflation, either, which you know is coming. And it is not just homes or beach property. It includes stocks and family businesses. From the New York Times:

“For decades, assets were valued at the time of the owner’s death, even if the value had risen. This so-called step-up in basis rule works like this: If a stock that was bought for $1 is worth $10 when the owner dies, the gain is $9. But when that asset is passed on to heirs, the embedded gain is wiped out because the base value is now $10 and no capital gains tax is owed.

“This treatment applies to any asset, from liquid securities and private investment partnerships to a family home. If the total value of the estate is less than the current $11.7 million exemption level for an individual or $23.4 million for a couple, then no estate tax would need to be paid, either.

“A Biden administration may move to change this for logical and revenue reasons. At one point, the step-up in basis made sense. Imagine trying to determine the capital gains from AT&T stock that your grandmother bought in 1943 when record-keeping was done with a pencil and paper. Today, cost-basis information can be retrieved in seconds.

“But two different groups of people have raised concerns about losing the step-up loophole: the very wealthy and the moderately wealthy.”

Being allowed to keep your or your family’s own money is a “tax loophole.” And five Democratic US Senators, led by Cory Booker (D-NJ), are poised to lead the fight to end it.

“To build an economy that works for all Americans we must tackle the inequality in our tax system. The stepped-up basis loophole is one of the biggest tax breaks on the books, providing an unfair advantage to the wealthiest heirs every year. This proposal will eliminate that loophole once and for all. It’s time to stop subsidizing massive inheritances for the rich and start investing in everyday Americans,” said Senator Chris Van Hollen (D-MD).”

And some wealthy heirs are happy to be generous with your money as well.

“I could be called the poster-child for the stepped-up basis. The Disney stocks I own have dramatically increased in value, but if I were to pass them on to my kids without selling them? No one would ever pay taxes on that. That wealth doesn’t disappear, so I don’t know why the responsibility to pay taxes on it should,” said Abigail Disney, member of the Patriotic Millionaires.”

And thanks to budget and reconciliation rules in Congress, Republicans can’t stop them with the filibuster. It will only need 51 votes - every Democratic Senator and the Vice President (if we can pry her away from her southern border duties) to become law, along with similar unanimity in the House, where Democrats currently only have a 3 vote margin. And it appears he can offer up as many reconciliation bills as he needs to pass tax bills. At least Senate rules will not allow them to include eliminating the Electoral College, making the District of Columbia a state, or increasing the size of the Supreme Court. For now.

Reading about the likely tax provision raises a question: whose money do the Democrats think we’re talking about? They seem to think all money is the government’s, and they’re letting you keep some of it. After all, they clearly believe that they can spend it better than you. It doesn’t take long before that extends into private property. Your pensions and IRAs may be next.

Biden will sign whatever is put in front of him. Cover your wallet and consult your financial and tax advisors sooner than later. Especially if you’ve done the responsible thing and built some savings, invested wisely, took risks to build a family business or two, and saved some money to pass along to your kids and grandkids, most of it without the help of a government program, and often in spite of them.

They’re coming after you and your money. No good deed goes unpunished. Elections have consequences.